Being surrounded by business students who strive for high finance jobs, I can say anecdotally that people think working in the insurance industry is extremely boring. I would be lying to you if I did not think the same coming into freshman year of college. However, I had the opportunity to do research for a professor looking at Insurance-linked Securities (ILS) as a freshman and found there to be a lot of interesting developments happening in the industry, especially in relation to climate change. Recently having attended the ILS NYC 2024 conference, I thought it would be worthwhile to talk about this growing industry. In this article, I want to give an overview of CAT Bonds as well as give some insights about what I learned at the conference.

The Reinsurance Industry and Cat Bonds

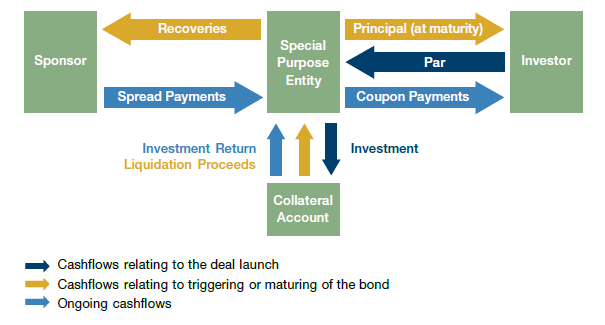

Reinsurance is insurance for insurance companies and plays a huge role in keeping the insurance industry afloat in the scenarios of large losses. But just like an insurance company, it must take care of its balance sheet and creditworthiness as it is highly sensitive to large events like climate disasters. Over the past five years, Moody’s stated that there has been on average $100 billion worth of global insured natural catastrophe losses. This has caused insurance and reinsurance companies to limit coverage or exit certain markets, with examples in the U.S being floods in Florida and wildfires in California. In addition, when costly climate disasters occur, property catastrophe reinsurance rates will substantially rise, with reinsurance companies taking on higher attachment points and aggregate covers becoming less. This will decrease the capacity of reinsurance companies as there becomes an asset-liability mismatch with perhaps their assets side being unable to cover for the large liabilities losses. Therefore, CAT bonds have been great instruments to help transfer some of this risk that reinsurance is supposed to take on to the capital markets. Below is a simple diagram from Man Group of how a CAT Bond works.

To start, the sponsor will enter a reinsurance agreement with a SPV to collect capital from investors. This capital will then be used to issue the bond into the secondary market, where investors will be able to purchase it. A collateral account will be used to help collect the proceeds from investors and be invested in securities that have high-credit rating to ensure “guaranteed” payments. Because of this, CAT bonds do not carry any credit risk, which is attractive to insurers to know that there will never be an instance of non-payment on a claim. Now, a CAT bond can be triggered through generally two ways: indemnity or parametric. Indemnity is the most common trigger and just looks at aggregate damages done, while parametric looks into weather factors like wind speed or total amount of rainfall as the trigger. If the trigger occurs, the sponsor will be able to get the funds initially invested by investors, whether partial or full. If not, the investor gets all its principal back at the maturity of the CAT bond plus the coupon payments that come with it.

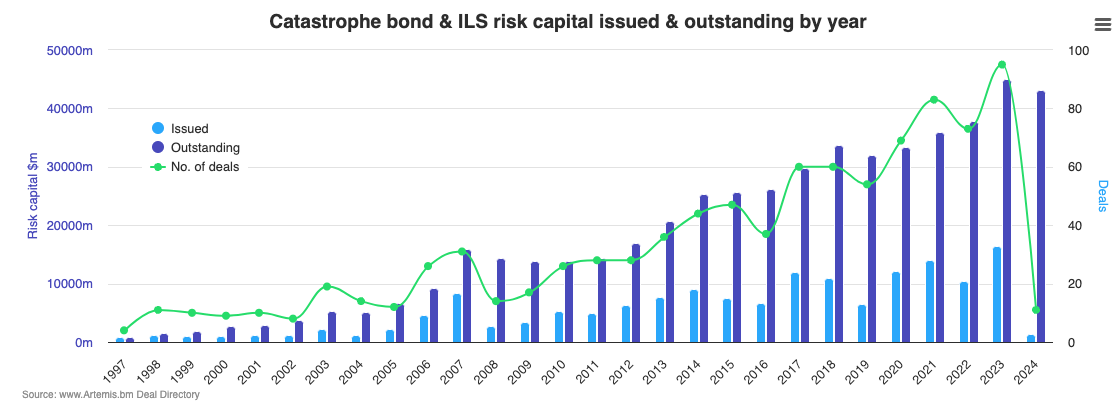

With large climate catastrophe events being very low frequency, it is important that reinsurance companies take on a long-term view of their balance sheets. If there are so few players in the space, rates will be driven down as these companies will start underwriting short-term reinsurance. But if a major event occurs, it may affect the industry’s capacity to provide sufficient coverage. This is what makes CAT bonds so interesting. Because property and casualty (P&C) insurance will inevitably grow with the frequency of climate events and the need for capacity, my thesis is that this instrument will have to grow as balance sheets of these insurance companies are constrained from a risk perspective. Sure, they may have the capacity to underwrite more, but they may have reached their max risk exposure. So far, the market growth is set to soar for CAT bonds, with an estimated $20 billion of insurance being forecasted by GAM Investments in 2024, which would be greater than the phenomenal 2023 year of Cat bond issuance. Below is a better visualization of Cat bond issuance and amount outstanding.

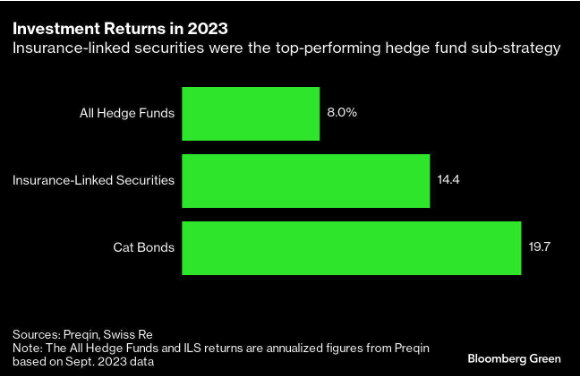

As I have been following CAT bonds since freshman year, it was a surprise to see them starting to make headlines and become more discussed within financial markets by the end of last year. For some of the top hedge funds that specialize in ILS investing like Fermat Capital Management and Leadenhall Capital Partners, it was a fantastic 2023 year for them and was spurred due to some factors like extreme weather events and high costs of rebuilding after natural disasters. Below is a graph to showcase hedge funds returns and the dominance of ILS and Cat Bonds for 2023.

This should be illustrative of the opportunity that CAT bonds present for investors seeking alternative sources for returns -- as an investor, you can also do pro quota treaties as well but I will not be getting into that. Not only hedge funds, but family offices and PE firms like KKR have also been catching on to how the insurance sector can provide interesting diversified, low-correlated returns relative to the overall market for its investors. If high spread levels that were seen in 2023 can be sustained, I do not see a reason for why it should not be incorporated more into investors’ portfolios. As mentioned before, has a low correlation to the overall market and compared to other fixed income products, it has very little interest rate duration risk. It will be interesting to see what occurs for the year 2024.

NYC ILS Conference Overview

Being at the conference was quite weird, especially since I was one of only two people there who was an undergraduate student, let alone under the age of 30. However, it was definitely worth my time and I wanted to share some informative insights of what industry experts are thinking about regarding ILS securities.

To start with Cat bonds, there were many strong remarks about the exceptional performance of the asset class in 2023, with them mentioning huge inflows of money into this instrument by opportunistic investors amidst rising interest rates. However, that is not to say that all headwinds have vanished. Many of the speakers noted that normal allocations for investors into these ILS securities are a modest amount of 1-3%, largely due to the illiquidity and scalability that comes with such a strategy. This means that despite the outperformance of many large market indices, CAT bonds will still need more than one year evidence that it can be part of investors’ portfolios. There was also recognition that ILS investors have also become more sophisticated over the years, especially given the fact that many have been following the asset class for at least a decade. Therefore, better climate risk modeling will be needed to provide evidence that capital should be given to CAT funds over pure capital strategies like equities or fixed income. So as interest rates start to fall and spreads tighten, it will be important to build transparency with investors in terms of pricing and predictability of interest-payments. Also, large left tail risk events are a reason why investors may be wary of allocating capital into these strategies, with them skeptical of climate risk modeling being done. In addition, poor asset-liability management from reinsurance companies that we saw more occur starting with the rise in the Fed Funds rate in March 2022 showed decreasing book values of these companies, meaning less underwriting and hurting the inflow of capital into CAT bonds. The final thing to note is that CAT bonds have largely been only open to institutional investors’ capital, so it will be important in the future to help retail investors obtain exposure to this growing asset class to help fill in demand.

Despite my fascination towards Cat bonds, the most interesting topic of the conference was the Cyber bond, which is an extremely new instrument that was only introduced last year. As the world becomes more and more interconnected, cyber risk becomes an even larger problem. Cyber (re)insurers will have to serve a huge role in being able to measure the impact and frequency of these events, despite the lack of historical loss data. For 2023, there were four 144A Cyber bonds issued and will secure about $415 million in protection for those sponsors, showcasing the start of what can be an important tool for firms to minimize cyber risk. As Richard Gray of Breazley stated at the conference, there will be a need for capacity, but it is extremely important that investors are educated and confident in the cyber modeling. Because this is such a new area of expertise, despite the similarities to CAT bonds in terms of structure, indemnity traits, and catastrophic tail risk, cyber modeling companies like CyberCube must be transparent in how they think about trends. This is definitely an area worth reading about and I am starting to do more research on this instrument for perhaps future articles.

Thank you for reading and hope you enjoyed learning a bit more about the developments happening in the insurance industry.

Sources

Evans, Steve. “Around $20bn of Catastrophe Bond Issuance Possible, Market Growth Could Soar.” Artemis.Bm - The Catastrophe Bond, Insurance Linked Securities & Investment, Reinsurance Capital, Alternative Risk Transfer and Weather Risk Management Site, 20 Feb. 2024, www.artemis.bm/news/around-20bn-catastrophe-bond-issuance-possible-market-growth-could-soar/.

Evans, Steve. “Family Offices Leaning into Insurance for Diversification. so Is KKR: Mcvey.” Artemis.Bm - The Catastrophe Bond, Insurance Linked Securities & Investment, Reinsurance Capital, Alternative Risk Transfer and Weather Risk Management Site, 13 Feb. 2024, www.artemis.bm/news/family-offices-leaning-into-insurance-for-diversification-so-is-kkr-mcvey/.

Evans, Steve. “First Cyber Cat Bonds a Watershed Moment: Moody’s RMS Video Interview.” Artemis.Bm, 30 Jan. 2024, www.artemis.bm/news/first-cyber-cat-bonds-a-watershed-moment-moodys-rms-video-interview/.

Lee, Sheryl Tian Tong, et al. “The World Being on Fire Is Swelling ‘catastrophe Bonds’ to a Record $45 Billion-and It’s a Key Hedge Fund Strategy.” Fortune, Fortune, 22 Jan. 2024, fortune.com/2024/01/21/hedge-funds-climate-change-catastrophe-bonds-disaster-insurance-record-high/.

“Property Catastrophe Reinsurance Market Dynamics to Slow in 2024.” Fitch Ratings: Credit Ratings & Analysis for Financial Markets, 23 Nov. 2023, www.fitchratings.com/research/insurance/property-catastrophe-reinsurance-market-dynamics-to-slow-in-2024-23-11-2023.

“Reinsurers Defend against Rising Tide of Natural Catastrophe Losses, for Now.” Moody’s | Better Decisions, www.moodys.com/web/en/us/about/insights/data-stories/reinsurers-mitigate-lower-profits.html. Accessed 23 Feb. 2024.